Why is this important

The “Bank Activity Index” rating is an attempt to systematize and compare the stability, efficiency, and quality of commercial banks’ operations using a unified methodology. Such comparisons increase sector transparency and give the market an indication of which banks are currently stronger in key areas — from mediation and accessibility to asset quality and liquidity. Against the backdrop of the growth of lending and deposits in the IV quarter of 2025, the rating update shows how banks are looking in the context of increasing competition and changing operational structure.

What happened

- The Center for Economic Research and Reforms presented the updated rating of banks based on the results of the “Bank Activity Index” for the IV quarter of 2025.

- The study covered 35 commercial banks and divided them into two groups — large and small — with separate leader tables and dynamics.

- Based on the results of the quarter, point shifts were noted in both groups: some banks improved their positions, others decreased, while a significant portion of participants retained their positions.

Numbers and facts

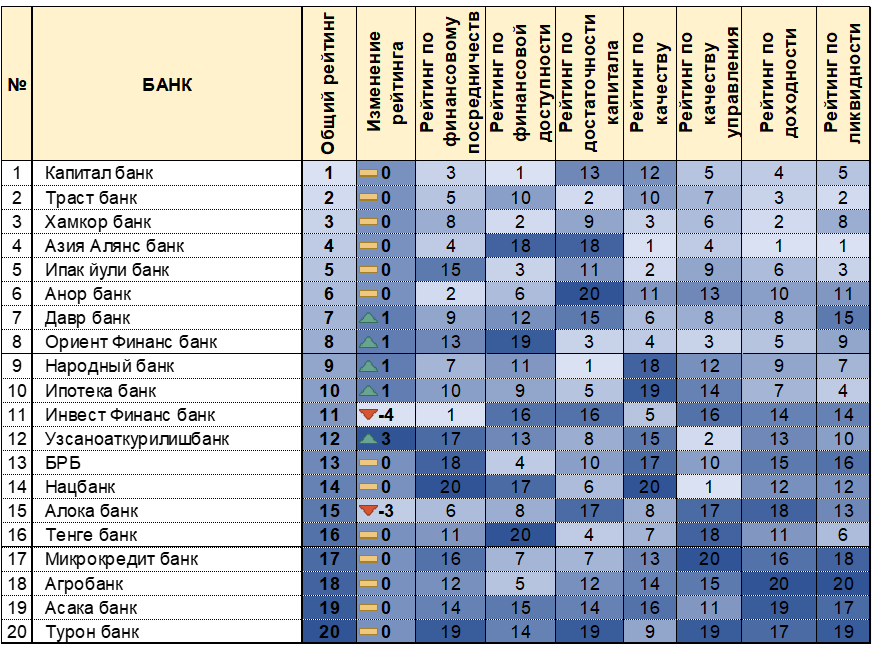

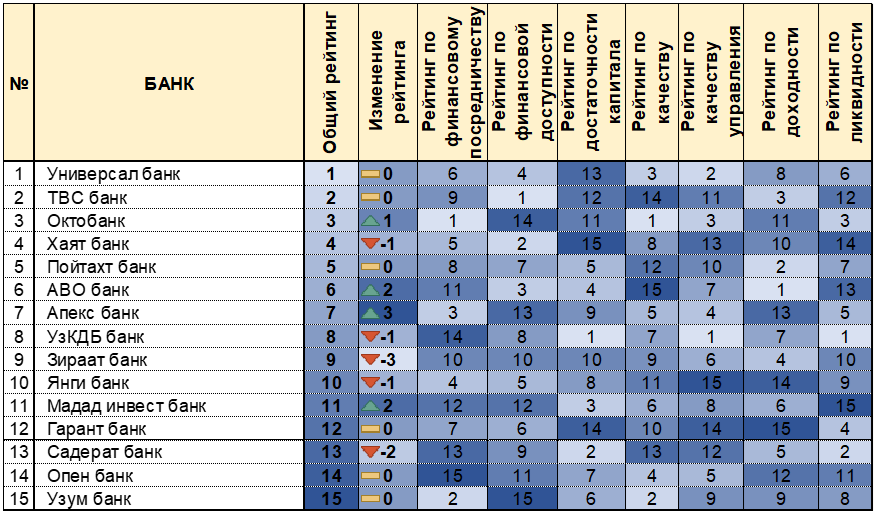

- The rating was compiled for 35 commercial banks: 20 large and 15 small.

- The methodology is based on 27 indicators comparable to the national average and international standards, including the requirements of the Basel Committee.

- Financial results of the IV quarter of 2025 by sector: assets — 892.9 trillion soums ($74.2 billion), liabilities — 759.8 trillion soums ($63.1 billion), net profit — 13.5 trillion soums ($1.1 billion) (+57.1% year-on-year).

- Dynamics: lending +13%, deposits +31%; the share of problem loans decreased to 3.5% compared to 4.3% a year earlier; capital adequacy exceeds the minimum standards by more than 1.4 times.

Large banks

- Growth: Davr bank (+1), Orient Finans bank (+1), Xalq bank (+1), Ipoteka bank (+1), Uzsanoatqurilishbank (+3).

- Decrease: Invest Finans bank (−4), Aloqa bank (−3).

- Unchanged: other banks — 0.

Small banks

- Growth: Octobank (+1), AVO bank (+2), Apex bank (+3), Madad Invest bank (+2).

- Decrease: Hayot bank (−1), UzKDB bank (−1), Ziraat bank (−3), Yangi bank (−1), Saderat bank (−2).

- Unchanged: Universal bank, TBC bank, Poytaxt bank, Garant bank, Open bank, Uzum bank – 0.

Context

- The picture for two groups shows “stability with point shifts”: the upper positions are generally maintained, and the main movements occur within the middle segment.

- For large banks, the sharp declines of individual participants, as well as the fact that some banks can simultaneously improve overall ratings but lose positions in individual indicators, appear to be a noticeable signal — this indicates the heterogeneity of the profile within a single organization.

- For small banks, the dynamics appear more “vivid” in the middle of the table: several players rose by 2-3 positions at once, while one bank lost three positions at once, reflecting this group’s sensitivity to changes in mediation and profitability.